Housing crisis finally pushes Canada's economy into recession

The long-anticipated, but delayed, recession on the Canadian economy has finally arrived, according to a new report by Oxford Economics.

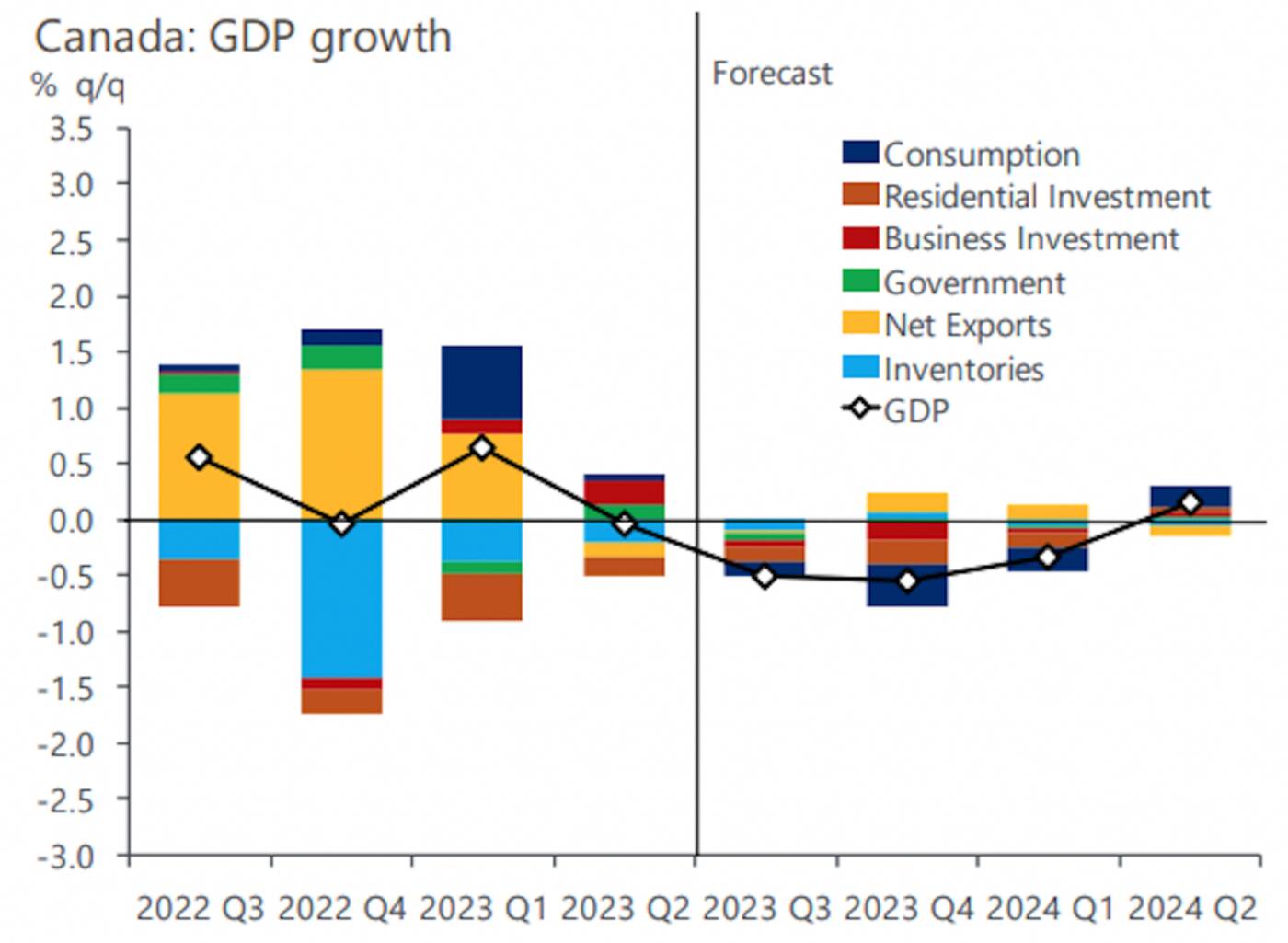

Highly indebted households and overvalued home prices are the driving factors leading to a pullback in consumer spending, which has slowed significantly since early 2023 — even with strong immigration, strong job growth, and the remaining spending spree backed by excess pandemic-time savings.

The recession was originally expected to hit in the fourth quarter of 2022, but the economy performed much better than anticipated.

"We doubted the economic strength at the start of this year would last, and the latest data indicates that a hard landing is indeed coming," reads the report.

"We expect highly indebted households will cut spending as they deleverage and pay down debt, which should put the principal portion of the debt service ratio on a downward trajectory. Rising interest costs will therefore account for the bulk of higher debt service costs, and likely even greater than our current forecast when factoring in the impact of extended amortizations for variable rate mortgage holders."

Households have already begun to cut back on buying new cars, furniture, appliances, and services due to debt service costs, job losses, and lower disposable income.

Household consumption accounts for 60 per cent of Canada’s GDP, and it will be the primary drag on the economy, but analysts forecast a 1.3 per cent decline in consumer spending during the recession, which is smaller than the decreases in previous recessions due to immigration, post-pandemic pent-up demand, and excess pandemic savings.

Canada GDP forecast. (Oxford Economics/Haver Analytics)

The recession started with the GDP drop in the second quarter of 2023, and it is expected to end in the first quarter of 2024, with a 1.5 per cent peak-to-trough decrease in GDP.

The unemployment rate is expected to increase from 5.5 per cent today to 7.2 per cent by the middle of 2024.

This is a relatively limited decrease as it is expected employers will prefer to retain their staff by cutting working hours, given the immense challenges of scaling up their staffing emerging out of the pandemic.

Major new fiscal stimulus programs are not expected to be introduced by the federal government, as it would inflationary pressures and undermine the Bank of Canada's monetary policy to date of sending the policy interest rate to 5 per cent.

The federal government is also challenged with emerging out of the deep red in its budget, with a target of balancing its books by 2027/2028.

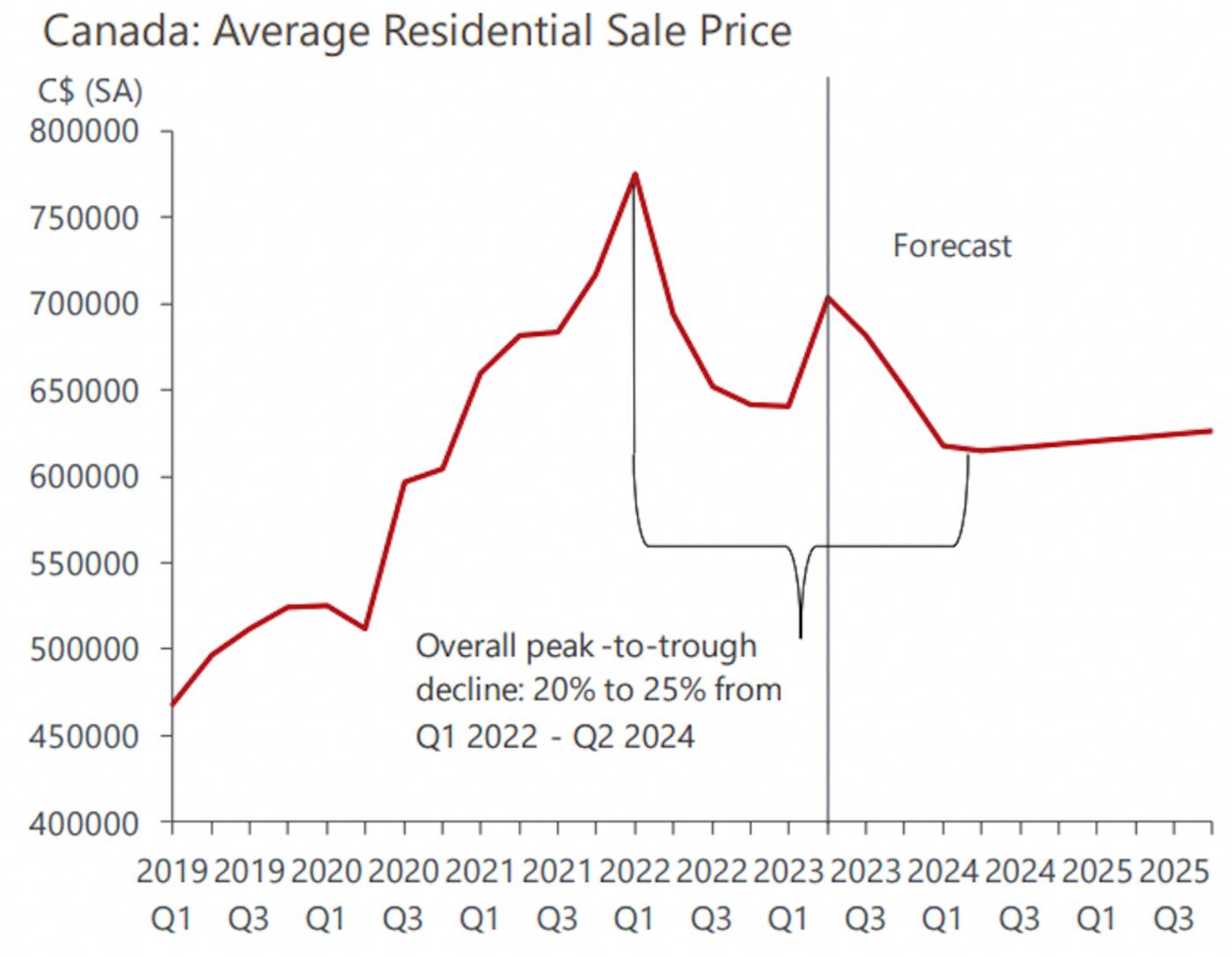

As for the real estate market, Oxford Economics predicts the housing correction is still far from over.

There was an upswing in resale home prices starting in February 2023, but the correction resumed "in full force" over the summer, which is expected to continue into 2024 as the recession unfolds.

Job and income insecurity combined with higher mortgage rates and record unaffordability will weaken housing demand even more, leading to a further drop in home sales.

Home prices will fall by another 5 per cent to 10 per cent by the middle of 2024, leading to an overall 20 per cent to 25 per cent drop in home prices since February 2022 — just before the Bank of Canada's first policy interest rate increase.

Canada home price forecast. (Oxford Economics/Haver Analytics)

There has also been a slowdown in new home construction, which is now expected to fall further as the recession progresses.

Housing starts are expected to reach about 220,000 units in 2023 and 200,000 in 2024 — well below the average of 270,000 units annually in 2021 and 2022.

But home construction will pick up in late 2024, eventually reaching a record high of 310,000 housing starts in 2026, at which point the economy will have recovered, mortgage rates will have eased, and government measures encouraging new housing supply — such as removing GST from the construction cost of new secured purpose-built rental housing — will help make up for past shortfalls.

Fareen Karim

Latest Videos

Latest Videos

Join the conversation Load comments